Stay informed about the early stage investing ecosystem and the technology sector at large by browsing through cutting-edge reports from prominent organisations in the industry:

The 2025 European Deep Tech Report

The fourth annual European deep tech report. In a pivotal year for deep tech, how is Europe faring, and how has the breakout of AI influenced deep tech priorities and European deep tech credentials. Created in partnership with Lakestar, Walden Catalyst and Hello Tomorrow. Table of contents 1. DEEP TECH DEFINED – COMMON (MIS)CONCEPTIONS page 9 2. THE EUROPEAN DEEP TECH OPPORTUNITY page 28 3. FUNDING LANDSCAPE page 40 4. SEGMENT DEEP DIVES – BIGGEST TRENDS page 51 NOVEL AI, FUTURE OF COMPUTE, NOVEL ENERGY, SPACE TECH, RESILIENCE, COMPBIO & CHEMISTRY, ROBOTICS 5. FOUNDER RESOURCES page 171 6. CHALLENGES & RECOMMENDATIONS page 180

PitchBook Analyst Note: A Lack of Pathway From US CVC Investments to an Eventual M&A

The CVC paradox: High investment activity, low acquisition rates by corporate sponsors Corporate venture capital has been an undisputed force in the US venture ecosystem. Since 2014 it has accounted for more than 46% of total VC deal value and 21% of deal count. Yet despite having deployed massive capital, CVCs haven’t converted many of their portfolio companies into acquisitions. PitchBook’s latest analyst note examines 25 years of CVC activity, exploring the reasons why M&A may not be the end goal for many of these investors. Senior analyst Kaidi Gao lays out some of the strategic and financial considerations for these investors and how a changing M&A landscape may impact potential CVC-backed acquisitions in 2025 and beyond. Table of contents Key takeaways 1 Introduction and methodology 2 Why US CVC investments have not led to many M&As 4 Case studies 9 Outlook 12

Founder Ownership Report 2025

Executive summary Every startup begins with an idea. And that idea begins with the founding team. In some cases, that founding team is one individual—a solo entrepreneur with an appetite to do it all. In other cases, the team includes multiple co-founders who hope to use their complementary skills to conquer a market. In the beginning, the founding team typically owns all of the startup’s equity. But this state of affairs rarely lasts for long. From the outset, deciding how to divide equity among co-founders, investors, employees, and other stakeholders is a strategic choice—and it remains critical as a company continues to grow. This report uses anonymized data from more than 45,000 startups incorporated from 2015 through 2024 to shed new light on how founder ownership works across the U.S. venture ecosystem, digging into first-of-its-kind data on the composition of founding teams, how founding teams divide their initial pool of equity, and how equity ownership evolves as startups move through their fundraising journeys. How should a company spend this precious equity resource? We hope this data can help founding teams and their investors as they consider this question at every stage of the venture-backed journey. Report highlights Solo founders are stepping up: The percentage of all startups incorporated on Carta that are led by a solo founder has more than doubled over the past decade, reaching 35% in 2024. Over this same span, startups with three, four, and five founders have become less prevalent. Solo founders are less likely to raise VC funding: Compared to larger founding teams, solo founders are less successful in raising venture capital. While solo founders comprised 35% of all companies incorporated in 2024, they accounted for just 17% of all companies launched in 2024 that also closed a VC round before the end of the year. Equal equity splits are becoming more common: While most founding teams choose to divide equity among themselves on an unequal basis, a growing number of co-founders are opting for an even split. In 2024, 45.9% of two-person founder teams divided up their equity equally, compared to 31.5% back in 2015. Founder ownership declines most at early stages: After raising a seed round, the median founding team collectively owns 56.2% of their startup’s equity. At Series A, that figure falls to 36.1%, and at Series B, it’s 23%.

Guides to Cross-border Investing in Early-Stage Startups | Estonia, Finland, Slovenia

The following 3 pdfs offer in depth guides and recommendations for cross border investing in early stage startups. Each country offers unique opportunities and faces unique challenges, making the differentiating guides an excellent resource for tailored and structured recommendations for helping you become a successful cross border investor Slovenia’s startup ecosystem, while compact, boasts global success stories like BitStamp and Outfit7. With a strategic location in Europe, the country bridges Eastern and Western markets. Its tight-knit community, supported by accelerators, incubators, and a growing network of investors, makes it a fertile ground for innovative startups aiming for international expansion Download the Guidebook Known for its world-class innovation and strong engineering heritage, Finland is a leader in sectors like gaming, health tech, and AI. Iconic names such as Supercell and Wolt emerged from its collaborative ecosystem. With events like Slush and Arctic15, Finland offers a vibrant platform for startups and investors to connect Download the Guidebook Despite its small size, Estonia punches above its weight in the global startup scene, producing unicorns like Skype and Bolt. With a digital-first approach, including e-Residency, Estonia makes it easy for international founders and investors to thrive. Its supportive policies and efficient digital infrastructure foster rapid growth and innovation Download the Guidebook

Foundation Startups in Greece report 2024-2025

The report provides an in-depth look at the Greek startup ecosystem for 2024-2025, highlighting key trends, investments, and emerging sectors like AI and green technologies. It explores funding challenges, gender disparities, and initiatives such as HDBI and Elevate Greece that are driving innovation and global competitiveness. An essential resource for understanding Greece’s entrepreneurial landscape. Download the Full Report Here

Capital Markets Union – Key Performance Indicators 7th Edition

The Association for Financial Markets in Europe (AFME), in collaboration with eleven other European and international organisations, has published the seventh edition of the “Capital Markets Union – Key Performance Indicators” report, tracking the progress of Europe’s capital markets against nine key performance indicators and analysing the progress over the past seven years. Among the key findings of the 2024 report on European capital markets’ performance: EU Capital Markets Falling Behind: Despite some cyclical gains, the EU lags behind the US, UK, and China in most key indicators, such as access to capital, global interconnectedness, and market liquidity. The EU’s capital markets remain fragmented, undermining economic competitiveness on a global scale. ESG Leadership, but Growth Slowing: The EU continues to lead in sustainable finance, with ESG bonds accounting for 13% of total bond issuance in 2024, ahead of the US and UK. However, growth in EU ESG issuance has not kept pace with growth in non-ESG issuance, with the overall share of ESG issuance down from 15% in 2021, signalling a potential plateau. Deteriorating Intra-EU Integration: The report highlights a worrying decline in financial integration within the EU, a trend also noted by the European Central Bank. This fragmentation threatens the EU’s overall financial stability and its ability to compete globally.EU Securitisation Market Remains Underdeveloped: The EU securitisation market continues to trail behind those of the US, UK, and Australia. Currently, only 1.9% of outstanding EU loans are transformed into securitised vehicles or loan sales, compared to 7% in the US, 2.8% in Australia, and 2.2% in the UK. Issuers from only 9 of the 27 EU member states utilised securitisation as a source of funding in the first half of 2024. Widening Market Disparities: Northern European nations, such as Luxembourg and the Netherlands, boast deeper capital markets and greater access to finance, while countries in Eastern Europe lag behind. This disparity poses a significant challenge to the EU’s ambition for an integrated capital market. EU FinTech Ecosystem Stalling: Private investment in EU FinTech remains lower than in the US and UK, limiting the region’s progress in digital finance. However, the EU has taken a leadership position in the issuance of tokenised bonds, accounting for 20% of the global market in this emerging area. Download the Report

The State of European Tech

We happily share with you the 10th anniversary edition of the State of European Tech presented by atomico. This report outlines a data-driven analysis of the trends, challenges, and opportunities shaping European tech over the past decade. For more information on this report you can visit: https://www.stateofeuropeantech.com/ Download the report below: Download The Report

EBAN 25th Anniversary History Book

25 Years of EBAN Since its establishment in 1999, it has been our privilege and honour to drive the growth of the early-stage investment and entrepreneurial ecosystem across Europe and beyond. Over the past 25 years, through numerous programmes, initiatives, and events, EBAN has facilitated the creation of a more integrated innovation value chain, enabling smart capital, corporations, governments, and innovators to collaborate more effectively and synergistically. Through its Network, Events, Communities, EBAN Academy, Research and Advocacy work, the association has positioned itself as a leader in connecting angel ecosystems across borders, setting standards and best practices in the market, fostering knowledge-sharing among diverse stakeholders and representing the interests of the asset class. Now heading into its 26th year, We want to celebrate this important milestone and many of the achievements made to date through this publication. Download the EBAN 25 Years History Book here

Building a Vibrant Business Angel Ecosystem in Europe

Building a Vibrant Business Angel Ecosystem in Europe Recommendations for EU and National Policy Makers This Policy Recommendation Paper addresses key issues facing the EU’s startup ecosystem, particularly the lack of funding and regulatory barriers that push many startups to relocate during the scale-up phase. Despite Europe’s innovation potential, early-stage investments are limited. The paper calls for streamlined regulations, cross-border funding incentives, and stronger government support to boost business angel investments and improve liquidity for startups. Aligned with Mario Draghi’s competitiveness strategy, it offers actionable recommendations to ensure the EU remains a global leader in innovation and technology. We identify 7 key areas that need to be addressed by the EU: To see more and learn about the actions we recommend to fix these issues, download the full paper below! Fill the form below to subscribe and download the paper Email* When you submit the form, check your inbox to confirm your subscription Name* Surname* Organization* Privacy* I´m authorizing EBAN (The European Trade Association for Business Angels, Seed Funds and Early Stage Market Players, located in Brussels, 1040 BE) to save and use my personal data according to the General Data Protection Regulation (GDPR). This information is used by EBAN exclusively for sending newsletters and other email campaigns about the latest developments in the global entrepreneurial, innovation, and early-stage ecosystem. Subscribe and Download

EBAN Annual Statistics Compendium for 2023

EBAN presents the EBAN Annual Statistics Compendium for 2023, Europe’s most extensive annual research on the activity of business angels and business angel networks. The Compendium offers comprehensive insight into the overall early-stage market, shedding light on the operational dynamics of business angel networks and providing valuable insights into their investment attitudes. Drawing from a wealth of sources, including European business angel networks, Federations of BANs, and data from prominent platforms such as Dealroom.co, Crunchbase, PitchBook, and the European Commission, the report offers a nuanced perspective on the entrepreneurial landscape. This report covers 38 countries on the European continent, the figures presented in the report, while not representative of the entire European market, provide valuable insights into the trends and developments shaping the early-stage investment landscape. Fill the form below to subscribe and download the report Email* When you submit the form, check your inbox to confirm your subscription Name* Surname* Organization* Privacy* I´m authorizing EBAN (The European Trade Association for Business Angels, Seed Funds and Early Stage Market Players, located in Brussels, 1040 BE) to save and use my personal data according to the General Data Protection Regulation (GDPR). This information is used by EBAN exclusively for sending newsletters and other email campaigns about the latest developments in the global entrepreneurial, innovation, and early-stage ecosystem. Subscribe and Download

4NGELS Guidebook: Cross-border Investments into Early-Stage Startups in Estonia

This guidebook walks you through the whole Estonian startup-investment ecosystem. This is good use for investors outside of Estonia or local investors who are interested in becoming an angel investor. The guidebook is put toghether in 2024 so all the information presented was valid around this time. 4NGELS is an international angel-investor education project with an aim to encourage cross-border investing into Estonia, Finland, Poland and Slovenia. In the guidebook you’ll get information about Estonia – the land of unicorns, gain insight about local startup ecosystem, useful information about how to find deal flrow, what to take into account culturally, what are local strenghts and challenges, legal information, success stories and emerging trends. The guidebook is free and you are welcome to download it.) Download the guidebook here

The Future of European Competitiveness

Get the latest on the Future of European Competitiveness presented by the European Commission. In Part A 2 this programme goes over how to tackle the innovation deficit that is taking place throughout the continent. You can read an excerpt of the detailed report below Read the Full Report Excerpt from Part A.2 of the report: A better financing environment for disruptive innovation, start-ups and scale-ups is needed as barriers to growth within the European markets are removed. While high-growth companies can typically obtain finance from international investors, there are good reasons to further develop the financing ecosystem within Europe. Very early-stage innovation would benefit from a deeper pool of angel investors. Ensuring sufficient local capital to fund scale-ups would concentrate the spillovers of innovation within Europe. Increasing the appeal of European stock markets for IPOs would improve funding options for founders, encouraging more start-up activity in the EU. To generate a significant increase in equity and debt funding available to start-ups and scale-up, the report proposes the following measures. First, expanding incentives for business “angels” and seed capital investors. Second, assessing whether further changes to capital requirements under Solvency II are warranted, which establishes capital adequacy rules for insurance companies, and issuing guidelines for EU Pension Plans, with the aim of stimulating institutional investment in innovative companies in selected sub-sectors. Third, increasing the budget of the European Investment Fund (EIF), which is part of the EIB Group and provides finance to SMEs, improving coordination between the EIF and the EIC, and eventually rationalising the VC funding environment in Europe. Finally, enlarging the mandate of the EIB Group to enable co-investment in ventures requiring larger volumes of capital, while also enabling it to take on more risk to help “crowd in” private investors.

2024 H1 Review by Sifted – Europe Sheds Some Downturn Ghosts

Compared to the previous 6 months in 2023, the first half of 2024 is seeing a resurgence of investments within the European tech ecosystem. Around €47.3bn, which includes €18.7bn debt funding has been injected into European startups in H1. This staggering amount is indicative of the demand for high quality talent and innovative products that are being pushed by VCs, public funds, and banks. Get the latest reporting of these from Sifted as they complied their H1 review on investments made throughout the continent.

Center for Venture Research: THE ANGEL MARKET IN 2023: AN INFLECTION POINT FOR WOMEN ANGELS?

The angel investor market in 2023 exhibited an increase in active investors, but a decline in the number of investments and the total dollars invested by angels, according to the Center for Venture Research at the University of New Hampshire.

LEAPFUNDER: State of the Startup Market Report Q1 2024

During each quarter Leapfunder prepares a State of the Startup Market Report and have just issued Q1 of 2024. In this report they go over developing startup hubs in Germany and the Netherlands while also mentioning new arrivals in their Startup Directory. You can also find valuable insights when reading through their interview with Sabine Schoorl, senior partner at LUMO Labs and startup coach since 2013. Get the latest updates in this report rendition and stay up to date on the new up incoming startups.

AEBAN: Annual 2023 Report

AEBAN presents its VIII Annual Report on the activity of Business Angels in Spain during the year 2023, prepared by the team of the Business Angels Network of the IESE Business School. This report will explain that the aggregate data of early-stage direct investment activity shows a clear decrease in investment in 2023. This decrease is more significant in mature stage projects, where the scarcity of foreign investment has been especially felt. Find the full report in Spanish and an excutive summary report in English.

EstBAN: Investment Summary 2023

Once a year, the Estonian Business Angels Network conducts a survey among its members, asking investors to share their investments made during the year. Last year in 2023 they have found that the same level of investments have been made, which has proved favourable especially given the continuation of the war in Ukrain and the current economic environment. In this report you will find in which sectors the most common types of investments being made and the changes in where they have been made geographically. Find these insights from EstBAN network in the full report here:

FiBAN Press Release: 30% decrease in angel investments and increase in bankruptcies

The Finnish Business Angels Network (FiBAN) reports a significant decline in angel investments in Finnish startups during 2023, with funding dropping from €37 million to €26 million compared to the previous year. This 30% decrease reflects the cautious stance adopted by investors amidst uncertain financial markets. In this report, FiBAN goes over how this decrease effected the various funding rounds of startups, as well as the distribution of invesments and exits by region. To learn more about the current state of the Finnish investment market you can find the full report below.

Investors Portugal: “Early Stage Investment Barometer 2023”

Lisbon, February 5, 2024 – Eight out of ten (79%) Portuguese early stage investors are dissatisfied with public policies for the sector. According to the “Early Stage Investment Barometer 2023”, the first survey of the sentiment and perspectives of investors in the Portuguese ecosystem, carried out by the Portuguese Association of Early Stage Investors– Investors Portugal, 21% rate the evolution of these measures very negatively, This analysis will go into further detail into Portuguese investor sentiment towards the recent policies and trends that are prevelant throughout Portugal. To get more access to these premier insights you can read the full report down below

Survey of Czech Startup Investors | 2023

In the ongoing effort to support and develop the Czech startup ecosystem, EBAN member Depo Ventures are providing you with exclusive and extensive data from business angels, LPs, GPs, and potential newcomers who participated in their survey of startup investors in Czech Republic. Find a link below to the full report in English.

European Data Insights report

Our partner Carta is a proud sponsor of the freshly-released European Data Insights. Read full report here.

State of Gender Diversity in European Venture report

Our partner Carta is a proud sponsor of the freshly-released State of Gender Diversity in European Venture report – the most comprehensive analysis of the funnel of female innovation in Europe. Read the full report to discover unprecedented levels of data on the investment opportunities to back female entrepreneurs and emerging fund managers in Europe.

Business Angel Guide to Investment in the SpaceTech Sector

The European space sector benefits from being diverse, robust, and enjoying rapid growth in recent years. European nations have a long history of cooperation in space research, technology development, and satellite deployment and the European space sector encompasses a wide range of activities, including satellite manufacturing, launch services, Earth Observation (EO) applications, broadcasting satellite services, global navigation solutions, and space exploration ventures. In this handbook, we will explore the key players, trends, risks, and opportunities to provide Business Angels, who are not yet operating in the sector, with the basic information to assess and explore investment opportunities in the space sector.

State of the European Tech Report

The State of the European Tech executive summary encapsulates the most crucial data points of the year. Delving into key indicators of the ecosystem’s health, it meticulously spotlights both favorable aspects and challenges. The narrative articulates a central thesis for the year: the imperative for the entire ecosystem to commence embracing risk in order to shape the future. Key findings reveal that global investment levels have experienced a notable decline, reflecting a market reset that extends beyond European borders. Projections for the total investment volume in 2023 indicate a decrease to less than half of the peak seen in 2021 across all global regions. Contrary to a global slowdown, Europe emerges as a leader in producing new tech founders, surpassing the United States consistently over the past five years. Despite a heightened threshold for entering entrepreneurship, the annual volume of founders initiating new tech startups in Europe exceeds that of the US. Following a downturn that resulted in a $400 billion reduction in ecosystem value, there has been a significant rebound, bringing the total ecosystem value back to $3 trillion. This resurgence is attributed to a robust recovery in public markets, elevating Europe’s value to its historical peak. You can read or download the report here:

EBAN Annual Statistics Compendium for 2022

EBAN presents the EBAN Annual Statistics Compendium for 2022, Europe’s most extensive annual research on the activity of business angels and business angel networks. The Compendium offers comprehensive insight into the overall early-stage market, shedding light on the operational dynamics of business angel networks and providing valuable insights into their investment attitudes. Drawing from a wealth of sources, including European business angel networks, Federations of BANs, and data from prominent platforms such as Dealroom.co, Crunchbase, PitchBook, and the European Commission, the report offers a nuanced perspective on the entrepreneurial landscape. This report covers 38 countries on the European continent, the figures presented in the report, while not representative of the entire European market, provide valuable insights into the trends and developments shaping the early-stage investment landscape. Fill the form below to subscribe and download the report Email* When you submit the form, check your inbox to confirm your subscription Name* Surname* Organization* Privacy* I´m authorizing EBAN (The European Trade Association for Business Angels, Seed Funds and Early Stage Market Players, located in Brussels, 1040 BE) to save and use my personal data according to the General Data Protection Regulation (GDPR). This information is used by EBAN exclusively for sending newsletters and other email campaigns about the latest developments in the global entrepreneurial, innovation, and early-stage ecosystem. Subscribe and Download {{ vc_btn:title=Download+Statistics+Infographic&style=flat&color=danger&align=center&link=url%3Ahttps%253A%252F%252Fwww.eban.org%252Fwp-content%252Fuploads%252F2023%252F12%252FInfographic-Updated-post-summit-27.11.23-1.png%7C%7Ctarget%3A%2520_blank%7C }} {{ vc_btn:title=Download+EBAN%27s+Statistics+Compendium+2022&style=flat&color=danger&align=center&link=url%3Ahttps%253A%252F%252Fdrive.google.com%252Ffile%252Fd%252F1Ej66IXC5lUNjyaIqyKvfQaBRs_2ukWSv%252Fview%253Fusp%253Dsharing%7Ctitle%3ADownload%2520EBAN%27s%2520Statistics%2520Compendium%25202022%7Ctarget%3A%2520_blank%7C }}

EBAN Data Report: Business Angel Networks and Angel Federations in Europe 2023

This report by EBAN provides a list of all Business Angel Networks and Federations currently active in Europe. It has been compiled through a combination of online resources and data providers such as our partner Dealroom, as well as Pitchbook, Gust, National Business Angel Network listings, Social Media Platforms, reports by EBAN Members, and more. Currently, there are 358 organizations identified by EBAN as active Business Angel Networks or federations spread across 37 countries. A full breakdown of organizations per country can be found in the report. The purpose of this report is to provide a better overview of the Business Angel Networks and Federations ecosystem in Europe. Read or download the report here: v

EIF Venture Capital Survey 2023 : Market sentiment, scale-up financing and human capital

The EIF VC Survey and the EIF Private Equity Mid-Market Survey (the largest combined regular survey exercises among General Partners on a pan-European level) provide an opportunity to retrieve unique market insights. This publication is based on the results of the 2023 VC Survey, conducted by the EIF with the support of Invest Europe. The paper focuses on the market sentiment as well as on issues related to scale-up financing and EU strategic autonomy. The study looks at the current situation, developments in the recent past and expectations for the future. It highlights substantial challenges, but also opportunities as perceived by survey participants. The main results are summarised and compared over time. The publication provides a valuable picture of the developments in the VC market in 2023 as well as an outlook for the near future. The EIF Working Papers are designed to make available to a wider readership selected topics and studies in relation to EIF´s business. The Working Papers are edited by EIF’s Research & Market Analysis and are typically authored or co-authored by EIF staff or are written in cooperation with EIF. You can read the full study here.

Capital Markets Union Key Performance Indicators – Sixth Edition 2023

The Association for Financial Markets in Europe (AFME) and EBAN, in collaboration with ten other European and international organisations, has today published the sixth edition of the ‘Capital Markets Union – Key Performance Indicators’ report, tracking the progress of Europe’s capital markets against nine key performance indicators. This year’s report shows a mixed picture, revealing no discernible medium-term advancement on the CMU key performance indicators. This edition also coincides with the 30th anniversary of the Single Market. Here too, the data points show minimal change in the development of the EU’s capital markets on a global scale.

Patents, trade marks and startup finance – Report by EUIPO

Patents, trade marks and startup finance This study examines the role of intellectual property (IP) rights – specifically patents and trade marks – in facilitating access to finance for European start-ups. To this end, it assesses the links between the filing of IPRs by start-up firms and their success in raising venture capital (VC), as well as the signalling power of patents and trade marks as predictors of successful exit strategies for investors. Main findings On average, 29% of European starts-ups have filed registered IP rights, with important differences between industry sectors. Biotechnology is by far the most IP-intensive sector, with nearly half of start-ups using patents or trade marks. Start-ups increasingly make use of IP rights as they grow, with a strong focus on European IP rights at all growth stages. The fiing of patents and trade marks at the seed or early growth stage is associated with a higher likelihood of subsequent VC funding. This effect is particularly important at the early stage, with a 4.3 times higher likelihood of funding for start-ups that filed trade marks, and a 6.4 times higher likelihood of funding for start-ups that filed patents. Start-ups that filed both trade marks and patents show the highest likelihood of funding at both the seed and early stages. The filing of European patents and trade marks is associated with an even higher likelihood of subsequent VC funding for start-ups. The filing of patents and/or trade marks is associated with a more than twice higher likelihood of successful exit for investors. The highest likelihood of Initial Public Offering (IPO) or acquisition is observed for start-ups that filed both patents and trade marks.

Best Practices of Angel Investing

Best Practices of Angel Investing Exciting News from Dealum! Dealum has just released their latest project, a FREE online book titled “Best Practices of Angel Investing.” This comprehensive guidebook is a valuable resource for angel investors, startup enthusiasts, and anyone looking to navigate the world of early-stage investments. Key Highlights: ● Learn how to manage investor groups for optimal outcomes efficiently. ● Tips and tricks for due diligence and spotting the red and green flags in startup investments. ● Explore the power of community and networking in the startup ecosystem. ● Discover how to make impactful, ethical investments that drive both profit and positive change. The best part? It’s available for FREE to anyone interested in angel investing. Knowledge is power, and Dealum is sharing it with the world.

FiBAN Startup questionnaire 2023

FiBAN publishes the results of their startup questionnaire sent to startups who have sought funding through the FiBAN. The goal of the questionnaire was to acquire information about improving the overall startup experience and to understand the profile of applying startups. FiBAN’s feedback and the overall experience were considered mostly positive, though pointed out some communicative development points in our process. Most startups who applied ended up receiving funding even if not via FiBAN. Most still recommend FiBAN as a funding channel even though only 6% received funding through FiBAN’s dealflow.

NLC’s Health Impact Fund Initial Close

NLC’s Health Impact Fund is their latest flagship fund that aims to bridge this widening healthcare gap between innovation and the market. With a target size of €100 million, it will invest into a highly diversified portfolio of over 80 NLC ventures. Actively managed by NLC’s Fund Management (FM) team, the Fund will invest from the pre-seed stage when value creation and return potential are the highest, with the potential to allocate up to €9m per company in follow-on financing for the most successful ventures up until Series A and Series B. Their Health Impact Fund is the most diversified early-stage opportunity that addresses a major societal problem. The FM and the Health Impact Fund are registered with the Dutch Authority for the Financial Markets (AFM). More info below.

Leapfunder’s Startup Market Report Q2 2023

Are you interested in the state of the current startup market? Check out the report our member Leapfunder prepared for the Netherlands and Germany for Q2 2023. Read the full report below.

Emerging Tech Future Report: Generative AI

A new dawn in tech has arrived: The generative AI craze has taken hold—and it’s showing no sign of letting up. What does this new epoch mean for investors and the companies into which they pour their capital? Our latest analyst note, the Emerging Tech Future Report: Generative AI, dives into how the new technology may transform a range of verticals. PitchBook analysts who cover health, ecommerce, fintech, climate tech, and more weigh in on the opportunities in generative AI. Read the full report below.

The State of Adria Tech 2021-2022

Business angels of Slovenia were among the leading partners in preparing The State of Adria Tech report led by Silicon Gardens. The research examines tech companies that have received investments in 2021 or 2022 and have Slovenian, Croatian, or Serbian funders as active participants. The analysis unveils a remarkable growth in investments in tech companies within the Adria region, skyrocketing from around €300 million between 2016 and 2017 to an impressive €3.45 billion between 2021 and 2022. This exponential twelve-fold investment increase presents the region’s exceptional market development over the past five years. Moreover, there has been a five-fold increase in the value of exits and secondaries within the Adria region since the end of 2016, with a total combined value of €4.7B up to 2022. Furthermore, unicorns have escalated from one to six, providing additional evidence of the region’s enormous technological progress in recent years. In addition to these findings, it is noteworthy that regional tech companies that have successfully raised capital operate across a record number of industries. Besides, their extensive use of SaaS as a business model indicates regional tech companies’ impressive expertise in software development. However, the survey also highlights that most of the invested capital in the region comes from the USA (75%) and that the most successful tech companies in terms of operational performance and investment raise base their legal seats outside the Adria region. Read the full report below.

Austrian Investing Report 2022

With the Austrian Investing Report 2022, the pre-IPO investment activity in Austria was comprehensively examined for the first time. The knowledge gained now provides information about the investment motives and the behavior of both anglers and institutional investors. The report is intended to contribute to the design of conducive framework conditions for innovative start-ups. The order was placed jointly by the Austrian Angel Investors Association (aaia), the Austrian Private Equity and Venture Capital Organization (AVCO) and Austria Wirtschaftsservice GmbH (aws). Over 82 percent of the investors surveyed named the business model as a decision-making criterion for investments, and almost 73 percent named the technology. The main motive for investors is the return (21 percent). Supporting the founders (18 percent), enjoying working together (17 percent) and passing on know-how (12 percent) are also mentioned as motives not much less frequently. “The high focus on investments in Austrian growth companies is quite surprising. More than 56 percent of the shares are held in Austrian companies. That’s positive and important for the location,” says Dr. Rudolf Dömötör, Director WU Business Incubator. It is also interesting that according to the report, angel investors diversify more between individual forms of investment than institutional investors. Around 21 percent of the invested assets are in startups, scale-ups and spin-offs, 31 percent in real estate, 21 percent in stocks or bonds and 14 percent in SMEs and existing companies. Institutional investors, on the other hand, act with a stronger focus on startups, scaleups and spin-offs. These groups of companies account for around 77 percent of their invested assets. Read the full report below (in German).

DanBAN Investor Report 2022

The DanBAN member survey stands out for its ability to offer a comprehensive understanding of how private investors fund growth companies in Denmark, and it is unique in its approach to measuring impact. This is because all DanBAN members are required to participate, resulting in a 100% response rate and a survey of exceptional quality. Enforcing the reporting requirement entails losing 1-2 % of members each year due to non-compliance. Total investment: In 2022, Direct investments from DanBAN members of €60,6 mill. which is a new record and up 12 % from 2021. Vækstfondens BA-matching loans amounted to €18 mill, down from €19,8 mill in 2021. DanBAN members thus provided startup and early-stage companies with more than €78 mill. in financing in 2022. Read the full report below.

Practices of European Venture Capitalists

The European venture capital (VC) market picked up and proliferated after the 2008 economic breakdown but faced a sharp slowdown in the second half of 2022 and 2023. Starting the recovery from the impact of the Covid-19 pandemic, Russia’s invasion of Ukraine elevated geopolitical tensions and caused a global economic slowdown. As for many other industries, the increasing macroeconomic volatility, with rising inflation and supply disruptions, has severely affected the venture capital market. At the same time, groundbreaking changes are taking place in society, not least the emergence of new technologies, that create opportunities for VC investors. Artificial intelligence, blockchain, and deep-tech are just a few. The investor landscape for startups is also changing rapidly, with new types of investors entering the scene, such as new forms of corporate VCs, special purpose acquisition companies (SPACs), and super business angels. To get a better understanding of the VC landscape, leading European business schools and universities have joined their efforts and conducted a broad study of VC practices in Europe. In this report, they present their findings on how European venture capitalists select, value, and structure investment deals, what type of value-added activities they provide, and how successful they are with their investments. Read the full report below.

Business Angels in the Czech Republic in 2022

Czechs are among the most skilled investors in startups. Their strategies have generally been successful so far. Almost nine out of ten investors were able to make a profit on their investment, with nearly 12% making more than ten times their investment. Two-fifths of investors consider investing in startups more profitable than other forms of investment. These are the findings of a survey conducted by investment group DEPO Ventures, which is building a unique syndicate of angel investors in addition to angel funds. The survey was also conducted in partnership with the law firm Havel & Partners and the agency CzechInvest. The aim of this fourth annual survey was to map the environment of angel investing in the Czech Republic. Contrary to the widely accepted rule that a large percentage of startups fail, the survey suggests that investments have mostly been successful so far. About two-fifths of investors (41%) consider the performance of their investments in startups to be higher or equivalent to other asset classes. Exit has already been achieved in some of their investments by about 40% of investors, with the number of investors who sold their investments increasing by more than 10 percentage points compared to last year. Almost 86% of them sold their share at a profit. Investments were most commonly evaluated once to five times (51.4%). Read the full report below.

Business Angel Investing in Finland 2022

FiBAN’s annual study of investments and exits maps the development and impact of angel investments. In 2022, Finnish angels invested 37 million euros in 248 growth companies, says the latest study conducted by the Finnish Business Angels Network (FiBAN), collecting answers from 450 private investors out of FiBAN’s 670 members. 7% of FiBAN members’ investments were made outside of Finland. The most popular countries were Estonia, Sweden, and the United Kingdom. The median investment size remained at the level of 2021 at 20,000 euros. Less than ten percent of FiBAN’s angel investors make half of all investments made through the network. They are so-called super angels whose investments range from hundreds of thousands to millions of euros at a time. Read the full report below.

Discover Guide to Business Angels

Wondering how to protect your brand? This Discover Guide made by EUIPO in collaboration with EBAN will help you understand whether you have protection for your brand, and, if not, what actions you may want to take to protect it. Brand is often company’s most valuable asset and as such a lot of money is spent on designing, developing and promoting it. There is an assumption amongst many businesses that so long as they use it and register with the national/regional company register then it is theirs. However this is not the case. This Discover Guide will help you understand if you own your brand and if not what actions you might want to take to secure it. Who is this Guide for: All business who have created their brand and are either operating or plan to operate within the European Union.

NLC’s 2022 Impact Report

Get the news you need from NLC’s 2022 Impact Report. Laser-focused on healthtech innovation, NLC successfully built its 100th venture in 2022, aiming to connect much-needed early-stage technologies with patients. This Impact Report offers you easy-to-read infographics on impact, core market data and the founder’s personal note on his drive to change patient lives. Learn how NLC’s innovation achievements in healthcare, society and the environment contribute to the UN’s Sustainable Development Goals. Committed to bridging the market and innovation gap, NLC has set up the Health Impact Fund to continue delivering on its promise to patients: advance health, make impact.

The SICTIC Investment Report 2023

According to the Swiss ICT Investor Club (SICTIC) 2023 investment report, year 2022 turned out to be a very strong for venture capital in Switzerland. This growth was primarily driven by later-stage funding in non ICT sectors, with a few mega-rounds substantially bringing the total funding to a new record. The market segment relevant to SICTIC (early-stage ICT rounds) stagnated. Nonetheless, SICTIC investors contributed – once again – to nearly 70% of funding rounds in that segment, underlining the leading role of SICTIC as a matchmaking platform for early-stage startup investments. Top picks: 254 SICTIC Portfolio Startups raised a cumulative total invested capital of CHF 1.6B and created over 5000 jobs! SICTIC’s impact with 106 financing rounds is significant, with close to 70% of all early-stage ICT/FinTech Investments in Switzerland involving SICTIC Investors in 2022! Total investment received by SICTIC Portfolio startups CHF 1.6B Read the full report below!

EBAN Data – Agrifood sector in Europe

In this EBAN Data Monthly Report, we present an overview of the agrifood entrepreneurial and investment ecosystem in Europe (including Türkiye), with a focus on the investments in Agrifood companies in between 2020 and 2022, and the suggestions by EBAN to enhance private investment in Agrifood sector in Europe. In this report, we adopt FAO’s definition of “Agrifood” which covers “from agriculture production through to food consumption”. The analysis is supported by the data gathered through our partner Dealroom.co, a platform that gathers all publicly disclosed information on funding rounds made in Europe and beyond as well as through research on the literature, and the support of EBAN members who have contributed individually through interviews and as a group during the co-creation workshops. In Europe, private investment has been growing in the agrifood sector. Looking at the European VC rounds, investments in food startups increased 12 times between 2013 and 2020 and foodtech startup valuations increased 1.5 times between 2019 and 2020. Then, in only 1 year, between 2020 and 2021, investments in food startups have more than doubled . The effect of the COVID-19 pandemic is highly related to this increase. Focusing on the Business Angels investment in Europe, a significant growth can be seen in investment in food between 2019 and 2021, but the sector remains limited compared to the others, such as fintech and health. It is important to note that the agrifood investment and entrepreneurial ecosystem is developing at a different pace in different regions, even though it is central to the European economy.

Driving Equity: The Latest on Women in Innovation

Supernovas’ latest study found that the 2021-2022 period had seen the most venture capital investment in women-founded scale-ups with over USD 9 billion invested over those two years. European investors have been providing the largest share of VC capital for European scale-ups founded by women since 2020. But there’s still a lot of work to be done to reach a more equitable gender balance. Out of over 7 000 European scaleups, only 604 (8%) had at least one woman on their founding team. That’s why we continue to make women a central focus of our efforts. Findings reveal benefits of women in leadership and the barriers to their success Women-founded businesses are significantly more likely to focus on sustainability, with nearly 1 in 4 women-led scale-ups working to fight climate change Women-founded businesses converted a higher percentage of rounds from Seed to Series A (funding during the early stages of their business growth) in a shorter period of time than the European benchmark, but are still disadvantaged in late-stage investment rounds There is an especially high growth of women founded scale-ups in Austria, Germany, and Switzerland — they grew 16.6x since 2017 The full Supernovas study will be published 16 May

EBAN Impact Investing Report 2021 – 2nd Edition

EBAN Impact Publishes its 2nd Annual Impact Investing Report – Reporting on Investor Background and Investment Characteristics EBAN Impact is delighted to announce the publication of our 2nd edition of 2021 Impact Investing Report #EIIS2021. EBAN Impact is the home for all EBAN members interested in impact investing and social entrepreneurship. The Impact Investing Report provides information on the profile and background of impact investors, as well as the characteristics that define their investments. EBAN Impact’s Investing Report is based on a survey launched in April 2020 led by Juan Alvarez de Lara, board member of EBAN, chairman of EBAN Impact, and founder of Seed&Click, and sponsored by Dr. Lisa Hehenberger and Dr. Kai Hockerts, professors at ESADE Business School and Copenhagen Business School respectively.

The 2023 European Deep Tech Report by Dealroom

This report explores the latest trends in deep tech, VC, university spinouts, and more. It found that European deep tech startups raised $17.7B in 2022, a 22% decrease from 2021. The four main categories in deep tech are Novel AI, Future of Computing, Novel Energy, and Space Tech. Climate Tech also has a growing share of deep tech funding, from 6% in 2016 to 34% in 2022.

TNS Final Report: Unleashing innovation in the Mediterranean by Supporting 200 Startups

THE NEXT SOCIETY, a five-year project aiming to reinforce the innovation ecosystem in the Middle East and North Africa, supported 200 startups, 65% of which have a direct impact on SDGs. It helped 15 of these companies raise €700K+ in funding and 27 others create 85 jobs. This report summarises the project’s results and offers insights for future players in the region.

Private equity forecast: Europe’s investors brace for 2023

As the private equity industry emerges from a tumultuous 2022—marked by volatile macroeconomic conditions driven by soaring interests and geopolitical tensions—its participants are bracing for another challenging year. PitchBook reached out to dealmakers, investors, investment bankers and other service providers to get their take on what the industry will need to prepare for in 2023.

Impact startups – 2022 review

After a record year for impact startups in 2021, investment into the impact ecosystem is down 25% in 2022, with $57B raised globally. In 2022, impact investment in the US fell 36%, while Europeʼs final account for 2022 came in at +1%. Climate tech startups raised $44B in 2022, almost 80% of all impact funding.

The next generation of tech ecosystems

In their recent report dealroom.co analysed over 201 tech ecosystems. According to them, the coming years will be dominated by radical innovation and a need for next-generation types of tech ecosystems that can bring together entrepreneurship, patient capital, deep R&D, and science. So rather than measuring a status quo, this set of actionable benchmarks is meant as a tool to help ecosystems understand and measure their maturity and preparedness for the future.

Recessions, Resilience And Returns: Here Are 8 Tech Sectors Primed For Growth

According to Crunchbase, the global economy will fall into a recession in the first quarter of 2023 (if it’s not already). Recessions typically last 15 months (2008 was 18) followed by 48 months of expansion. With this publication Crunchbase endeavours to reveal which sectors will be the best and most resilient investment and growth in the coming months.

State of European Tech

Atomico published its ”State of European Tech” report: EU tech faces new challenges, but remains resilient. After a record-breaking first half year, the flywheel slowed this summer in response to a tough macro environment. But as the report reveals, opportunities and reasons to believe in European Tech remain. This paper also looks at Ukraine’s tech industry, which has underscored the role tech can play during times of crisis.

ACA Angel Funders Report 2022: More Data + Industry Insights and Real Stories

ACA publishes the Angel Funders Report annually to increase awareness about angel investor activity and build a deeper understanding of the investing environment. According to the 2022 report, ACA members invested $950 million in 2021 in more than 1,000 companies. On average, they invested a total of $5.3 million each, a 15% increase from 2020.

Capital Markets Union Key Performance Indicators – Fifth Edition by AFME

AFME, EBAN, and 10 other organisations published the fifth edition of the “Capital Markets Union – Key Performance Indicators” report. Over the last five years, this report has tracked the progress of Europe’s capital markets against nine key performance indicators. The 5th CMU progress report finds that the EU as a whole is falling further behind other jurisdictions in terms of its global attractiveness as a place for businesses to access deep pools of capital and go public. While there have been some considerable policy achievements over the last five years, including the EU maintaining its global leadership on sustainable finance and improving its FinTech regulatory ecosystem, our report shows there are several obstacles hampering the progress of the CMU.

How do the best business angels in Poland invest? – Polish angel investment market in 2021

The new Report on the angel market in Poland shows how this area of investment activity is shaping up. Venture Capital funds have been operating on the Polish market for a long time, but the sector of private investors is still at an early stage of development. The authors of the report estimate that there are currently 680 active business angels in Poland. In Western European countries there are usually at least several thousand. The results of the survey confirm that the angel investment market in Poland is still growing. As many as 40% of the surveyed business angels have been investing for only three years or less, and more than half of the business angels (53%) have made between one and six investments during their entire business angel activity. According to the report, investments in startups are, for the time being, the domain of men (80% of those surveyed), but the 20% share of female investors in the market is a result that stands out among European countries – Spain, Croatia, Latvia, Slovakia, Ireland or Finland have lower results. Business angels in Poland are mainly middle-aged, most of them are between 35 and 49 years old – this age bracket accounts for as much as 70%. To date, they have most often been entrepreneurs (55% of those surveyed) and corporate managers (30%). The report shows that these two professional groups are joined by doctors, lawyers, or IT professionals.

EIF Working Paper 2022/82, EIF Venture Capital Survey 2022: Market sentiment and impact of the current geopolitical & macroeconomic environment

The EIF VC Survey, the EIF Private Equity Mid-Market Survey, and the EIF Business Angels Survey (the largest combined regular survey exercises among General Partners and Business Angels on a pan-European level) provide an opportunity to retrieve unique market insights. This publication is based on the results of the 2022 VC Survey, conducted by the EIF with the support of Invest Europe. The paper focuses on the market sentiment as well as the impact of the current geopolitical situation and difficult macroeconomic environment. The study looks at the current situation, developments in the recent past and expectations for the future. It highlights substantial challenges, but also opportunities as perceived by survey participants. The main results are summarised and compared over time. The publication provides a valuable picture of the developments in the VC market in 2022 as well as an outlook for the near future. The EIF Working Papers are designed to make available to a wider readership selected topics and studies in relation to EIF´s business. The Working Papers are edited by EIF’s Research & Market Analysis and are typically authored or co-authored by EIF staff or are written in cooperation with EIF.

Global VC Pullback Is Dramatic In Q3 2022

Crunchbase Reports that Global VC Pullback Is Dramatic in Q3 2022: The big global venture capital pullback we were all expecting is truly here. Venture and growth investors in private companies scaled back their investment pace significantly as the slump in the public markets stretched into the third quarter. Venture funding for the third quarter of 2022 totaled $81 billion, down by $90 billion (53%) year over year and by $40 billion (33%) quarter over quarter, according to a Crunchbase News analysis. While funding for the most recent quarter will increase a little in the coming months as stealth fundings are announced, this is a huge drop in funding compared to prior quarters.

The open database for university spinouts

June 2022 database release The Spinout.fyi database is publishing its raw survey data, in order to level the information playing field for spinout founders who often enter negotiations not knowing what to expect. The database includes 143 unique entries from 71 universities from around the world. 47% of the universities are based in the UK, 37% in Europe, and 11% in the US. 41% of the spinouts raised Seeds, 17% raised Series As, 2% raised Series Bs, 15% were pre-funding, 3% no longer exist, 3% IPO’d, 7% exited via M&A. The universities covered by this survey include: Stanford University, Harvard University and Columbia University in the US; Oxford, Cambridge, Imperial, UCL in the UK; ETH Zürich and EPFL in Switzerland, Trinity College Dublin in Ireland, Ecole Normale Supérieure in Paris, and many more. The spinouts in the database cover a wide range of products, which we summarised into 6 categories: Software, Hardware, Therapeutics, Materials, Medical, and Diagnostics.

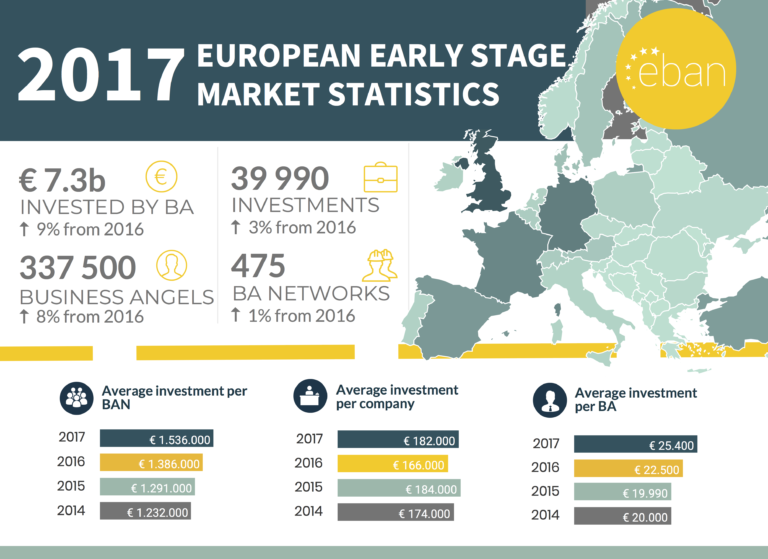

Statistics Compendium 2021 European Early Stage Market Statistics

EBAN Publishes its Annual Statistics Compendium – Reporting on the Activity of Business Angels and Business Angel Networks in Europe Data on the investments made across the 38 different European countries measured in the report indicates that the visible angel investment market on the European continent has grown substantially from the 767 Million Euros invested in 2020, to a record 1,456 Million Euros invested in 2021 (+90% from the previous year). In 2021, angel investors were involved in over 5070 observed funding rounds, consisting in both initial investments and follow-on investments made in European based start-ups. Based on the reports provided by national federations, local angel networks, and national venture capital associations, there are approximately 39400 active business angel investors on the European continent who are part of a local investment network or association. Fill the form below to subscribe and download the report Email* When you submit the form, check your inbox to confirm your subscription Name* Surname* Organization* Privacy* I´m authorizing EBAN (The European Trade Association for Business Angels, Seed Funds and Early Stage Market Players, located in Brussels, 1040 BE) to save and use my personal data according to the General Data Protection Regulation (GDPR). This information is used by EBAN exclusively for sending newsletters and other email campaigns about the latest developments in the global entrepreneurial, innovation, and early-stage ecosystem. Subscribe and Download {{ vc_btn:title=Download+Statistics+Infographic&style=flat&color=danger&align=center&link=url%3Ahttps%253A%252F%252Fwww.eban.org%252Fwp-content%252Fuploads%252F2022%252F10%252F2021-venngage-cropped.png%7C%7Ctarget%3A%2520_blank%7C }} {{ vc_btn:title=Download+EBAN%27s+Statistics+Compendium+2021&style=flat&color=danger&align=center&link=url%3Ahttps%253A%252F%252Fwww.eban.org%252Fwp-content%252Fuploads%252F2022%252F10%252FStatistics-Compendium-2021-FINAL-3.pdf%7Ctitle%3ADownload%2520EBAN%27s%2520Statistics%2520Compendium%25202021%7Ctarget%3A%2520_blank%7C }}

Women Angel Insights Report

New study reveals investments worth £2 billion made by female angels helping to create 10,000 UK jobs First comprehensive picture of female angel investment in the UK reveals thousands of female angels. More than £2bn has been invested in UK companies via deals involving female angel investors over the last 10 years, backing over 4,000 businesses and helping to create 10,000 jobs. New drive to attract fresh investment as figures show just 14% of angel investors are women. Almost 25% of all companies backed by female angels were female-founded, higher than the average of 19%. Female angel investors have helped drive more than £2bn of investment in companies across the UK in the past decade, a new study reveals today.

UNH Research Finds Angel Investor Behavior Can Be Influenced by Ego

UNH Research Finds Angel Investor Behavior Can Be Influenced by Ego Angel investors—wealthy individuals who provide essential funds for start-ups—often invest under conditions of extreme uncertainty. While their funds can be vital to early-stage ventures, researchers at the University of New Hampshire found that angels’ egos can play a significant role in their investment decisions—the bigger the ego, the larger and more diverse the deal and the lower the number of co-investors. Read the Press Release Read the Study

EIF Business Angels Survey 2021/22: Market Sentiment by EIF Research and Market Analysis

EIF Business Angels Survey 2021/22: Market Sentiment The EIF Business Angels Survey, together with the EIF VC Survey and the EIF Private Equity Mid-Market Survey (the largest combined regular survey exercises among GPs and Business Angels on a pan-European level) provide an opportunity to retrieve unique market insights. This publication is based on the results of the 2021/22 EIF Business Angels Survey. The paper focuses on the market sentiment and the impact of COVID-19. The study looks at the market situation, developments in the recent past and expectations for the future. The main results are summarised and compared over time. The publication provides a valuable insight of the developments and the markets in 2021/22, as well as an outlook for the near future. Read the Full Report

Q2 VC Funding Globally Falls Significantly As Startup Investors Pull Back by Crunchbase

Q2 VC Funding Globally Falls Significantly As Startup Investors Pull Back Global funding slowed dramatically in the second quarter of 2022 as investors shied away from later-stage funding bets. It also marked the first quarter with a significant drop in funding since the beginning of 2020. Funding reached $120 billion, the lowest amount recorded for a single quarter since the beginning of 2021, Crunchbase data shows. Read the Full Report

European Venture Report – Q2 2022 by PitchBook

European Venture Report – Q2 2022 European venture funding is on pace to surpass €100 billion for the second consecutive year, but dealmaking activity could slow as markets enter correction territory. In the Q2 2022 European Venture Report, Pitchbook explores the key trends that shaped the continent’s ecosystem in the first six months of the year. Read the Full Report

Ranking investors – EMEA 2022 by Dealroom.co

Ranking investors – EMEA 2022 40% of startups backed by top quartile investors go on to raise Series A, compared to just 7% for bottom quartile funds, and only the top 2% of funds have invested in two or more unicorns at Seed. Dealroom.co has brought purely quantitative analysis to the assessment of VC investors in EMEA, and why this ranking matters. Read the Full Report

Empowering European Digital Leaders: After Regulation, Let’s Quickly Promote Innovation by Euractive

Empowering European Digital Leaders: After Regulation, Let’s Quickly Promote Innovation Europe’s landmark digital regulation has laid the groundwork in record time for a new framework that will hold digital giants accountable and limit their monopoly position by dusting off competition law. After the General Data Protection Regulation (GDPR), the European Union is once again asserting itself as a normative power with the adoption of an unprecedented regulatory arsenal that lays down new obligations in terms of content management and competition: the Digital Services Act (DSA) and the Digital Markets Act (DMA). Read the Full Report

2021 Central and Eastern Europe Private Equity Statistics by Invest Europe

2021 Central and Eastern Europe Private Equity Statistics The 18th annual edition of the Central and Eastern Europe Private Equity Statistics delves into countries across CEE to show the spread of private equity and venture capital activity, as well as development of regional powerhouses. About Invest Europe: Invest Europe is the world’s largest association of private capital providers. They represent Europe’s private equity, venture capital and infrastructure investment firms, as well as their investors, including some of Europe’s largest pension funds and insurers. Read the Full Report

The Performance of European Private Equity Benchmark Report 2021 by Invest Europe

The Performance of European Private Equity Benchmark Report 2021 The research shows that European private capital continued to strongly outperform listed equity benchmarks, delivering superior performance to long-term investors to support pensions and savings as markets rebounded from the effects of COVID-19. About Invest Europe: Invest Europe is the world’s largest association of private capital providers. They represent Europe’s private equity, venture capital and infrastructure investment firms, as well as their investors, including some of Europe’s largest pension funds and insurers. Read the Full Report

The State of European Insurtech 2022 by Dealroom.co, mundi ventures, MAPFRE, NN Group

The State of European Insurtech 2022 This report wants to bring transparency through data and qualitative insights on the current state and trends of European and global Insurtech. The report has been has been developed by Dealroom.co, Mundi Ventures, MAPFRE, and NN Group, drawing on the partnersʼ collective insurance innovation expertise and insights from Insurtech innovators and leaders. Read the Full Report

The Angel Market in 2021: Metrics Indicate Strong Market – By Center for Venture Research

The Angel Market in 2021: Metrics Indicate Strong Market The angel investor market in 2021 exhibited an increase in active investors, the number of investments, and the total dollars invested by angels, according to the Center for Venture Research at the University of New Hampshire. Total angel investments in 2021 were $29.1 billion, an increase of 15.2% over 2020. A total of 69,060 entrepreneurial ventures received angel funding in 2021, an increase of 7.1% over 2020 investments. The number of active investors in 2021 also increased to 363,460 as compared to 334,680 in 2020, an increase of 8.6%. The deal size for 2021 increased by 7.6% from 2020, reflecting the higher valuations. For the second consecutive year the seed and start-up stage market were the predominant investment stage for angels. About CVR: The Center for Venture Research is a multidisciplinary research unit of the Peter T. Paul College of Business and Economics at the University of New Hampshire. The Center’s principal area of expertise is in the study of early stage equity financing for high growth ventures. Read the Full Report

Ukrainian ІТ Industry: Reboot in the Wartime – by IT Ukraine Association

Ukrainian ІТ Industry: Reboot in the Wartime The rapid growth of the industry by more than 50% during 2019-2021 continued up to the War and, according to the National Bank of Ukraine, in February 2022 reached the highest monthly indicator of export in the history of the Ukrainian IT market – $839 million, which is 43% more than for the same period in 2021 ($480 million). According to the results of 2021, the industry provided 37% in the export of computer services and USD 6.8 billion of the income to the economy of Ukraine, paid UAH 23.5 billion worth of taxes and fees. At the beginning of 2022, 285,000 IT professionals were working in the industry. During the first quarter of 2022, the IT industry provided record-high $2 billion of export income in wartime. A similar figure in 2021 was $1.44 billion. Therefore, the volume of IT exports has increased by 28%. In March 2022, the Ukrainian IT industry maintained 96% of computer services exports ($ 522 million) compared to the similar period last year ($ 546 million) and proved its resilience in the time of instability and increased risks.

Ukraine IT Report 2021 – by IT Ukraine Association

Ukraine IT Report 2021 In 2021, the Ukrainian IT industry grew by 36% from USD 5 billion to USD 6.8 billion in exports. At the same time, the number of specialists increased from 244 thousand to 285 thousand. Thus, over the past three years, the industry has more than doubled in exports and has grown by more than 50% in the number of specialists. The study used open data and information from state registers, as well as a survey of 98 Ukrainian IT companies, which by size correspond to the structure of companies participating in industry associations. Ukraine IT Report 2021 presents both short-term (up to one year) assessments and medium-term (until 2025) forecasts for the development of the IT industry, specialized education, as well as a comparison of Ukraine as an IT country with the neighboring countries. The study also provides data on the state of the office real estate market and the impact of Covid-19 on the format of work of the companies.

Ranked: The Most Prominent VC Investors in EMEA – 2022 by Dealroom.co

Ranked: The Most Prominent VC Investors in EMEA – 2022 Dealroom.co presents a practical ranking of venture capital investors, a tool to help founders navigate the vast, and at times opaque venture market, for each stage of their growth.

EBAN Impact Investing Survey

EBAN Impact Investing Survey We are proud to be driving research surrounding impact investing in startups that are dedicated to a societal or environmental cause. This is why we are supporting the EBAN Impact Investing Survey. That way we empower impact investors by giving them the data and the facts to make informed investments. Participate Here {{ vc_btn:title=Download+the+EBAN+Impact+Investing+Report&style=flat&color=danger&align=center&link=url%3Ahttps%253A%252F%252Fwww.eban.org%252Fwp-content%252Fuploads%252F2020%252F12%252FEBANIMPACTINVESTING2020-REPORT-2.pdf%7C%7Ctarget%3A%2520_blank%7C }}

Global M&A Report by PitchBook

Global M&A Report Global M&A activity bifurcated for much of Q1 2022, with previously negotiated deals closing on time while announced activity diminished due to the uncertainty created by Russia’s invasion of Ukraine, according to PitchBook latest Global M&A report.

European Venture Report by PitchBook

European Venture Report The Q1 European Venture Report takes a deep dive into the key trends that shaped this first quarter, breaking down activity across dealmaking, exits and fundraising, as well as regions. Highlights include: Late-stage VC continues to dominate deal value figures, accounting for 71.6% of total capital invested. Exit value plummeted from 2021’s heights amid a widespread tech public equity sell-off. VC fundraising got off to a solid start in terms of capital raised, but fund count dropped significantly

Number of Investments Made by EstBAN Members Tripled in 2021

EstBAN members invested 29.9M euros into startups, which is an all time high. From the total amount, 13.5M was angel investments, 14.9M through funds and 1.45M euros was invested through crowd funding.

France Angels, BILAN DES INVESTISSEMENTS 2021

France Angels presents the “Bilan des Investissements 2021”

Business Angels in The Czech Republic 2021

Depo Ventures presents Business Angels in The Czech Republic 2021 The aim of the report is to map the environment of the angel investing in Czech Republic. To find out how angel investors invest and what their problems are.

Foodtech Startups and Venture Capital – Q1 2022 by Dealroom.co

Amid war, supply chain volatility and an inflationary environment, the report dives into how the $1.1 trillion foodtech industry fared in Q1 2022, and where the $9.2B of VC investment raised this quarter was headed. Download the Report

Biannual Report on Financial Integration by European Central Bank

When we talk about euro area financial integration, we mean the extent to which financial services are available under the same rules and conditions in all countries that use the euro. In a well-integrated financial system, assets with the same risk-return characteristics cost the same, irrespective of the country in which they are traded. Financial integration therefore contributes to the uniform transmission of the European Central Bank’s (ECB) monetary policy across the euro area.

European Financial Stability and Integration Review

The European Financial Stability and Integration Review (EFSIR) is an annual review published by the European Commission. Among other topics, it reports on developments in finance, markets and banking, and has a special focus on financial stability.

Business Angel Investing in Finland 2021 by FiBAN

Investment activity of private startup investors reached a new high in 2021, following the decline of covid-year 2020. Majority of growth funding went to companies closing their first investment round. In 2021, private early-stage investors invested altogether 52,3M€ into 626 companies. Majority of the investments were placed in companies that received their first investment, shows FiBAN’s annual member survey, responded by 480 private investors.

Do We Need EU Social Taxonomy? By EVPA

Do We Need EU Social Taxonomy? By EVPA EU standards for sustainable finance can encourage investments that will enable a green and just transition, but only if they act as an accurate barometer and truly prevent green and social washing. Social taxonomy ABC. The European Commission’s Platform on Sustainable Finance published its final report on social taxonomy on 28 February. This comes in the framework of the EU’s legislative package on sustainable finance and EU taxonomy, which aims to create a common language for how companies and investors disclose green and social investments. Social taxonomy is about defining standards for social investments and for what activities contribute to achieving social objectives. This is important because the net zero transition will not happen without also taking social aspects into account: we need a green and just transition. Companies and investors cannot go ‘green’ whilst ignoring basic rights and decent working conditions. The transition needs to take place in “an economy that works for people” too. The report proposes a similar social taxonomy structure as the current green taxonomy: developing social objectives, defining types of substantial contributions, ‘do no significantly harm’ criteria; and minimum safeguards. It outlines 3 main objectives: decent work, adequate living standards and wellbeing, and inclusive and sustainable communities and societies.

In Search of EU Unicorns – What Do We Know About Them?

The Joint Research Centre (JRC), the European Commission’s science and knowledge service presents: In Search of EU Unicorns – What Do We Know About Them? This paper provides insights into the geographical and sectorial distribution of EU unicorns. Using the Unicorn club data from Dealroom up to mid-2021, it explores where they are located, how old they are and how they reached unicorn status. The analysis takes the form of a comparative study of unicorns from the EU, the US and China.

Invest in Software Companies

Invest in Software Companies – How to Assess SaaS Companies by Verve Ventures This report aims to give a framework for assessing SaaS companies and foster an understanding of this business model.

Sweden Tech Ecosystem: Report 2021

Dealroom.co presents: Sweden Tech Ecosystem: Report 2021 2021 was a record year for the Swedish ecosystem. VC investment more than doubled in the last year alone, hitting an all-time high of €7.8B. More on Sweden’s rise to the ranks as one of Europe’s leading startup ecosystems in our latest report made in partnership with Startup Sweden, The Swedish Agency for Economic and Regional Growth, Swedish Institute, Business Sweden and Vinnova.

Danish Biotech: a Rapid Rise

Dealroom.co present Danish Biotech: a Rapid Rise Covid provided a big publicity opportunity for biotech. Investors of all kinds started taking interest in the companies that had the power to shorten the pandemic, and save millions of lives, through things like vaccine development and rapid variant analysis. For Dansk Biotech’s spring summit, we dived into the rich emerging biotech ecosystem in Denmark, among the fastest-growing in the world. Download the Report

European VC Valuations Report

PitchBook presents European VC Valuations Report. European VC valuations continued to break records in 2021 across all stages as investors competed fiercely to participate in outsized rounds. Pandemic-induced growth for tech startups and an increase in nontraditional investors helped drive the astonishing climb in companies’ price tags. Our 2021 Annual European VC Valuations report takes an in-depth look at the key trends across stages, industries and regions that shaped valuations last year.

Emerging Venture Markets Report

MAGNiTT presents Emerging Venture Markets Report. With over $6.9B raised through 1,300+ deals and 80+ startup exits recorded, 2021 was a defining year for the Venture Capital ecosystem in Emerging Venture Markets.

Tackling the Scale-up Gap

Joint Research Centre (JRC) presents Tackling the Scale-up Gap The number of scale-up businesses in the EU, particularly unicorns, lags behind the US and China. This is partially attributed to a deficit in scale-up finance. Based on an a webinar between experts which took place on 5th October 2021, this paper reports and comments on the available evidence of the scale-up financing gap in the EU and discusses its causes and consequences.

Healthcare Predictive Analytics Market Overview

Deep Knowledge Group presents Healthcare Predictive Analytics Market Overview Healthcare Predictive Analytics market is projected to grow at a rate of 28.9% in terms of value, from USD 3.74 Billion in 2019 to reach USD 28.77 Billion by 2027. Healthcare Data Analytics companies secured almost $2.0 billion in venture capital funding in 2021 thereby showing the trend for future growth.

Navigating impact measurement and management – How to integrate impact throughout the investment journey

EVPA presents Navigating impact measurement and management – How to integrate impact throughout the investment journey which demonstrates how impact measurement and management is deeply embedded into the DNA of investing for impact and how it drives decision-making throughout the whole investment journey, from investment strategy to exit. This report also harmonises the work done by leading organisations in the impact ecosystem by clarifying the connections and complementarities among different IMM initiatives in each phase of the investment journey.

The State of European Tech

Atomico presents The State of European Tech, the most comprehensive data-driven analysis of European technology. What does Europe’s tech talent look like now? And how has Covid-19 affected the region’s tech hubs? Founders and companies have emerged resilient but their mental wellbeing has been tested to the extreme. Demand for talent has bounced back from the lows of spring. And virtual working has flung open the doors of the ecosystem and spurred the growth of emerging hubs.

Swiss Angel Investor Handbook

SICTIC, Swiss ICT Investor Club presents Swiss Angel Investor Handbook. This handbook is a condensed collection of wisdom from many successful angel investors, and will familiarize you with concepts of investing in seed and early-stage technology startups in Switzerland; help you learn the language that you’ll encounter in investment term sheets; point out 7 caveats and provide checklists that you can use when making your own startup investments.

Template Convertible Loan Agreement for Angel Investments